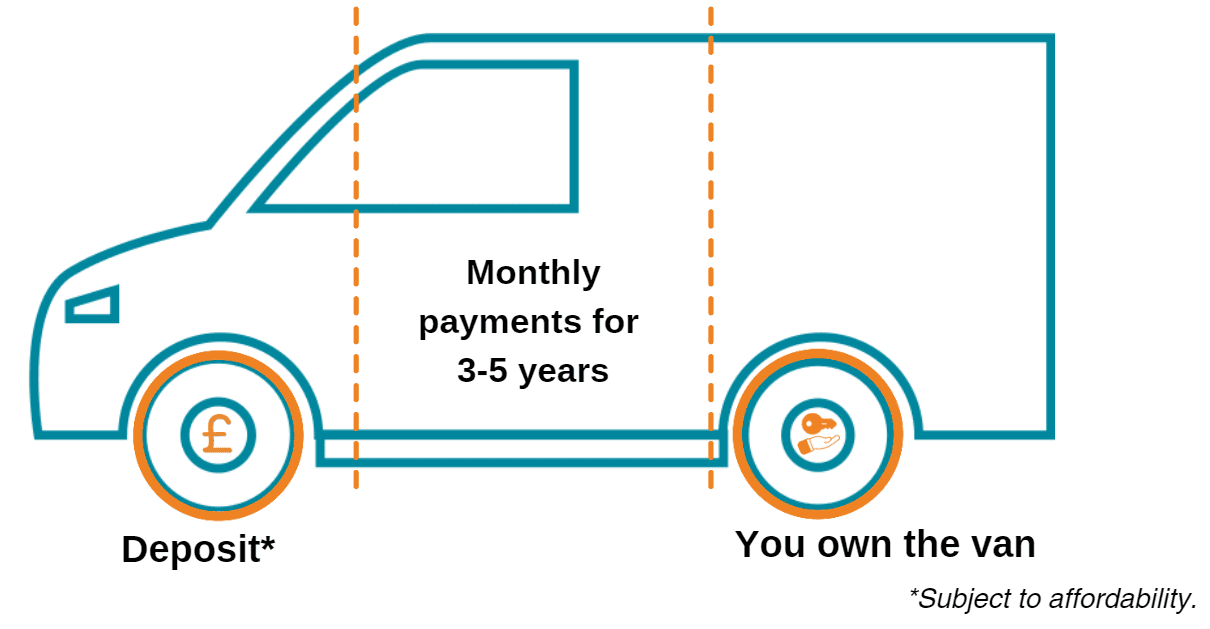

By putting down a deposit, you could afford a van that would otherwise be too expensive. This upfront payment can reduce the amount you need to borrow, allowing you to afford a bigger van or one with more modern features.

-

-

Car finance ›

-

‹ Back

-

TrustScore 4.4 | 16,009 reviews

-

-

‹ Back

-

Motorbike finance ›

-

‹ Back

-

TrustScore 4.4 | 16,009 reviews

-

-

‹ Back

-

Van finance ›

-

‹ Back

-

TrustScore 4.4 | 16,009 reviews

-

-

‹ Back

-

How it works ›

-

‹ Back

-

TrustScore 4.4 | 16,009 reviews

-

-

‹ Back

-

FAQs and guides ›

-

‹ Back

-

TrustScore 4.4 | 16,009 reviews

-

-

‹ Back

-

About us ›

-

‹ Back

-

TrustScore 4.4 | 16,009 reviews

-

-

‹ Back

-

TrustScore 4.4 | 16,009 reviews

-

Car finance ›

For a better road ahead

Moneybarn is a member of the Finance and Leasing Association, the official trade organisation of the motor finance industry. The FLA promotes best practice in the motor finance industry for lending and leasing to consumers and businesses.

Moneybarn is the trading style of Moneybarn No. 1 Limited, a company registered in England and Wales with company number 04496573. The registered address is Athena House, Bedford Road, Petersfield, Hampshire, GU32 3LJ.

Moneybarn’s VAT registration number is 180 5559 52.

Moneybarn No. 1 Limited is authorised and regulated by the Financial Conduct Authority (Financial Services reference No. 702780)